Waters Wrap: Big Tech, exchanges and a rapidly evolving market

Following LSEG’s partnership with Microsoft, Anthony talks with some industry participants to explore what this might mean for exchange tech going forward.

On November 9, 2021, after CME Group and Google signed a groundbreaking 10-year partnership/investment agreement, I wrote a column with this as the headline: “CME & Google—the first domino falls”.

The premise was hardly revelatory as the industry had been increasingly moving to the cloud for several years. What was clear, though, was that the exchange technology marketplace was about to undergo a massive shift. If the major exchanges were going all-in on cloud as the preferred infrastructure for trading, clearing and settlement, that meant that all market participants would have to start to ratchet up their own tech infrastructures so as to not fall too far behind the markets they trade into. (Which they have been doing—the Goldman Sachs-JP Morgan cloud initiative being a clear example.)

Sure enough, a few weeks after the CME-Google announcement, Nasdaq signed a similar partnership with Amazon Web Services (sans the investment). And while not as ambitious as those two aforementioned deals, this past July, Cboe Global Markets signed with Snowflake to improve its data and analytics capabilities (though there was no talk of multi-casting, settlement and clearing in the cloud).

Then this past week, London Stock Exchange Group announced a 10-year partnership/investment with Microsoft where “LSEG’s data platform and other key technology infrastructure will migrate into Microsoft’s Azure cloud environment.”

Sure enough, the dominos are falling…and there’s no end in sight.

In a report by Burton-Taylor International Consulting, which was put out after the LSEG-Microsoft news dropped, it noted that “exchanges have ramped up their commitment to cloud, spending $560 million in 2022 to incorporate cloud into their technology infrastructure,” and that “growth since 2019 has been 44% annually, with projected CAGR (compound annual growth rate) of 93% through 2025,” meaning that exchange spending on cloud is expected to exceed $1.6 billion over the next three years. (Click here should you want to ask for access to the full report. Lots of good survey-result tidbits in there and projections.)

To get a better understanding of how the exchange technology landscape is likely to shift in 2023, I spoke with a few people who have been watching these developments closely. Below are some theories, hopes, and a bit of reckless speculation. If you have your own ideas, I’d love to read them: anthony.malakian@infopro-digital.com.

* The most logical question in the aftermath of the LSEG announcement is, “Who will be the next domino and with which cloud provider?” The obvious exchange candidates are the Intercontinental Exchange (Ice), Deutsche Börse, Hong Kong Exchanges and Clearing Market (HKEx), Toronto Stock Exchange (TMX), or even Cboe going all in, rather than dipping a toe with data and analytics.

Sadly, I don’t have any inside information here, but for my money, I think it’s quite clear who the next domino should be—the Australian Securities Exchange.

Last month, ASX announced that it was halting its Chess blockchain replacement project, a failure that will cost the exchange to take an AUS$245-255 million (~$165-170m) pre-tax write-off, and which will also mean some layoffs and lost expense for industry participants, who were working in parallel to update their systems so they could feed into the new system that would use distributed ledger technology.

I’ve never been a fan of DLT (at least as it pertains to capital markets infrastructure technology), so I applaud ASX on making the tough decision to go in a new direction…and that direction needs to be toward the cloud. What better way to change the narrative than to hitch the market’s wagon to a name like Google, Amazon, Microsoft or IBM. (To put a twist on an old saying, you won’t get fired for picking IBM, but you might lose your job by going with a DLT startup.)

After talking with industry participants, it’s clear that ASX wanted to be seen as innovative by being a first-mover on ‘the inevitability of blockchain’. We’ve said it here at WatersTechnology many, many, many times before (just click the many links in this column), but cloud is the future, not blockchain. I don’t know what the sales pipelines are for the major American Big Tech cloud providers in Australia, but why put off the inevitable?

[Update: I had shamefully missed this, but back in October, ASX named Google Cloud “as its preferred cloud partner to build its data product innovation strategy.” Chess wasn’t mentioned specifically, but the release did state this: “The exchange is in the process of renewing several core platforms which will see the average age of the core equity market technologies drop from over 20 years to an average of less than five years.” So it’s worth keeping an eye on.]

* Brennan Carley, managing principal of Proton Advisors, a member of Sterling Trading Tech’s board of directors, and someone who spent a decade at Refinitiv/Thomson Reuters, says that the LSEG-Microsoft pairing should be of interest to two players, in particular—Bloomberg and Symphony.

First, BBG. As he wrote on Twitter, the deal “allows participants to pull up research notes, share documents, and type into a group chat all at once. Financial advisers will be able to do that using LSEG’s data with one screen.” Carley tells me that this is a direct shot at Bloomberg, but that’s only if—and it’s a big IF—LSEG can seamlessly integrate Microsoft Teams with Refinitiv’s Workspace platform (Eikon’s replacement).

Now, is Bloomberg really worrying about this as BBG killers have come and gone over the years, and also since an integration will take some time? It’s questionable.

“LSEG is not going to displace BBG in BBG’s core markets [of] fixed income and equities trading desks,” he tells me, “but they might get some of that business, especially in FX, where they have a strong franchise already, plus middle/back office and ‘off trading desk’ users, such as research, investment banking, etcetera).”

* Again, though, if the Teams-Workspace integration happens, that can lead to the creation of something like a “LinkedIn for the capital markets” play, which is something that it sounds like Symphony is working toward.

As such, Carley believes that this is “not great news for Symphony” because they are trying to compete with Teams as a collaboration and workflow tool for the capital markets. If Microsoft can tie in Workspace, that could be seen as a more valuable end-to-end data/collaboration/workflow offering than what Symphony has to offer. Also, the buy side loves Microsoft Excel, a segment that Symphony is still trying to win over (though, it should be noted, that execs at the vendor say they have been having increasing success at winning over asset managers and hedge funds).

But, again, if the Teams-Workspace integration actually happens and it leads to an enhanced Microsoft Excel experience, that would likely be very enticing for end-users.

* Let’s go out on a limb for a second: With the way this agreement was structured, that ~4% investment by Microsoft into LSEG allows Blackstone and Thomson Reuters (previous owners of Refinitiv) to sell down some of their stakes without putting downward pressure on LSEG’s share price, so it’s a win-win for all those involved.

Carley believes that because of the way the deal was structured, it could bring Microsoft closer to Blackstone, “which has a lot of portfolio companies that Microsoft sells to—and would like to sell more to,” he says.

* And to that point, Microsoft might’ve made this deal for a variety of reasons, and one of those reasons could be to get closer to Blackstone and its portfolio companies. So, the tech giant wants to expand its footprint in the capital markets (and not fall behind AWS/Google), which leads Carley to believe that it won’t look to take a bigger stake in LSEG, or else risk alienating other exchanges and data providers.

“The economics of the big tech vendors (meaning their financial criteria and business strategy) are oriented around massive, “horizontal” markets,” he says. “None of them have ever gone very deep (in terms of product offerings) into narrow vertical markets. For example, Microsoft doesn’t have a healthcare products division, a transportation products division, an entertainment products division; they do have marketing and sales teams organized by vertical, but in terms of product, at best, they do some minor tweaks or features to their standard products. That’s because their business models are optimized for massive scale, and as big as we like to think finance is, it is really a complex set of small markets—trading, research, investment banking, etcetera.”

Questions abound

* Someone else I spoke to is Robert Iati, managing director at Burton-Taylor, who has been predicting Big Tech’s takeover of the capital markets (and, specifically, of market data) for a couple of years now, and those predictions appear to be coming to pass.

He says that the Big Tech companies already have deep penetration into the capital markets, so now they are trying to increasingly carve out what their specialties are going to be.

“Google is everyone’s search engine; Microsoft owns the desktop software and is a big provider of servers (and [has a growing presence with its] Surface hardware now, too); and AWS is a cloud behemoth,” Iati says. “They are all eager to not only sell more of their cloud infrastructure, but they see the writing on the wall for the cloud as the next home for matching engines and trading systems. No entity in this business has more data than exchanges—orders, prices, executions—and cloud providers will benefit from its continued growth,” as it will help them to improve their machine learning capabilities, as the more data pumped into AI models can lead to more advanced correlations.

* Iati says that exchanges are seeing the long-term cost savings benefits that come with (proper) cloud migration projects.

“At a time when firms are positioning their data to ‘meet the clients where they are’, how better than to have a channel from Microsoft, Apple, Google to make it more available to do so?” he says. “Specifically from LSEG’s point of view, its acquisition of Refinitiv has not been met with cheers by the EU stockholders (or its press!). A deal like this illustrates how it plans to move forward, shows how it’s going to save money in the future, and offers more clarity into how it is going to leverage Refinitiv and its other data assets.”

I think the most interesting deal to come will not necessarily be, ‘Which exchange will be the next,’ but rather, ‘Which exchange will be the first to overlap and sign with AWS or Google [or, now, Microsoft]’ for the same services that are being done with Nasdaq and CME [and, now, LSEG].

Senior exchange executive

* With this latest deal, Iati believes “we’ve gone past the tip of the iceberg and I expect more such activity.” As a result, though, regulators around the globe are likely to increase their focus on cloud adoption, which is something that started even before these last few deals.

“I do wonder when regulators will see fit to influence similar deals and—as much as I am anti-regulation—install controls over the future of these,” he says. “While I’m sure the regulators were aware of this deal long before we were, it’s also a certainty that there are people in those Washington DC buildings that are salivating at the chance of limiting the way Big Tech gets into this business.”

And one more thing

* Finally, I was recently talking with a senior executive at a major exchange (but before the LSEG announcement). They noted that in these announcements, there hasn’t been any exclusivity (made public, anyway) in the way these deals are being structured—meaning (and Carley was talking about this, too) that they aren’t limiting themselves and can do similar deals with other exchanges. So, for example, Ice could team with Google, and Deutsche Börse could go with Microsoft.

“The question becomes, will the fact that these cloud providers have deals with their main competitors, will they want to sign similar deals for technology that will eventually be differentiating? I don’t know the answer to that, but I think the most interesting deal to come will not necessarily be, ‘Which exchange will be the next,’ but rather, ‘Which exchange will be the first to overlap and sign with AWS or Google [and, now, Microsoft]’ for the same services that are being done with Nasdaq and CME [and, now, LSEG],” the senior executive said.

Essentially, if/when that happens, then that will represent the true tipping point. While every trading firm—exchange or bank or large asset manager or vendor—is going to be “multi-cloud”, are they okay with teaming with someone on a specialized/customized/exclusive project that is also working on something similar with a competitor? If the industry gets comfortable with that idea, then all bets are off.

Again, if you have thoughts of your own or think anything said above is off base, feel free to reach out: anthony.malakian@infopro-digital.com.

The image accompanying this column is “Rock at Sea” by Raymond Jonson, courtesy of the Cleveland Museum of Art’s open-access program

Further reading

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@waterstechnology.com or view our subscription options here: http://subscriptions.waterstechnology.com/subscribe

You are currently unable to print this content. Please contact info@waterstechnology.com to find out more.

You are currently unable to copy this content. Please contact info@waterstechnology.com to find out more.

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. Printing this content is for the sole use of the Authorised User (named subscriber), as outlined in our terms and conditions - https://www.infopro-insight.com/terms-conditions/insight-subscriptions/

If you would like to purchase additional rights please email info@waterstechnology.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. Copying this content is for the sole use of the Authorised User (named subscriber), as outlined in our terms and conditions - https://www.infopro-insight.com/terms-conditions/insight-subscriptions/

If you would like to purchase additional rights please email info@waterstechnology.com

More on Emerging Technologies

Quants look to language models to predict market impact

Oxford-Man Institute says LLM-type engine that ‘reads’ order-book messages could help improve execution

The IMD Wrap: Talkin’ ’bout my generation

As a Gen-Xer, Max tells GenAI to get off his lawn—after it's mowed it, watered it and trimmed the shrubs so he can sit back and enjoy it.

This Week: Delta Capita/SSimple, BNY Mellon, DTCC, Broadridge, and more

A summary of the latest financial technology news.

Waters Wavelength Podcast: The issue with corporate actions

Yogita Mehta from SIX joins to discuss the biggest challenges firms face when dealing with corporate actions.

JP Morgan pulls plug on deep learning model for FX algos

The bank has turned to less complex models that are easier to explain to clients.

LSEG-Microsoft products on track for 2024 release

The exchange’s to-do list includes embedding its data, analytics, and workflows in the Microsoft Teams and productivity suite.

Data catalog competition heats up as spending cools

Data catalogs represent a big step toward a shopping experience in the style of Amazon.com or iTunes for market data management and procurement. Here, we take a look at the key players in this space, old and new.

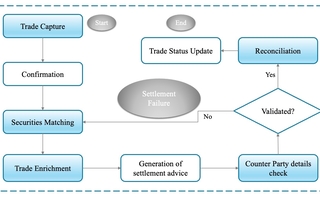

Harnessing generative AI to address security settlement challenges

A new paper from IBM researchers explores settlement challenges and looks at how generative AI can, among other things, identify the underlying cause of an issue and rectify the errors.